Specialist vs general AI agents for Debt Collection

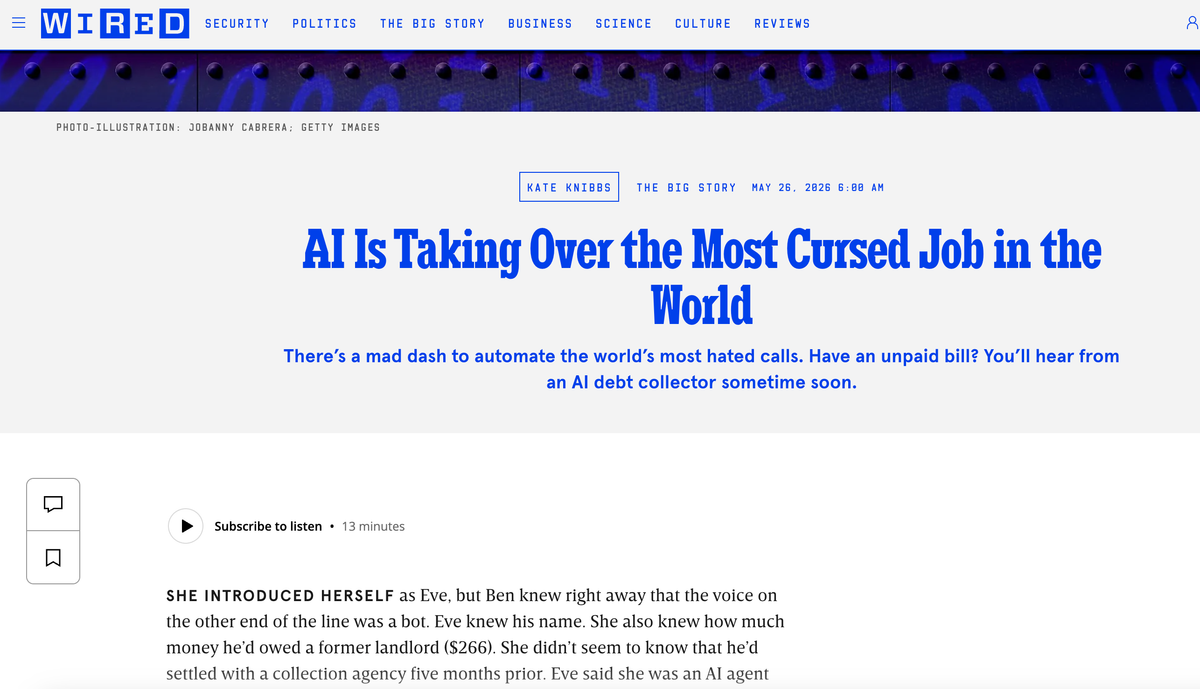

Wired reports US debt collection is being automated at extraordinary scale. London's Inicio AI offers a glimpse of what a more thoughtful version of the same technology can look like.

Wired published a fascinating piece this morning by Kate Knibbs on the AI agents now dialling Americans about their unpaid bills. If you have a few minutes, have a read to get an idea of how Conversational AI is being used in the debt collection sector in the United States.

The opening anecdote is both disappointing and fascinating: A man in Portland, Oregon, picks up the phone to "Eve", an AI agent from a collections firm who knows his name and a $266 debt owed a former landlord. The bot does not know he settled the debt five months earlier. He plays along, asks the bot to role-play, and eventually gets transferred to a human who confirms the balance is, in fact, zero.

Throughout the article, though, Kate highlights examples and instances that won't necessarily excite or delight anyone working in the Conversational AI industry. Think broken experiences - for example, one bot introducing itself with the customer's name rather than its own.

It's helpful to get a handle on some of the firms and metrics mentioned though. For instance, Kate highlights a startup called Domu, founded in 2023, now reportedly handling 70 million connected calls a month. Altur, another player, runs 2.5 million calls a month for clients including major Mexican banks. Floatbot has, according to the post, helped one healthcare collections client cut its human headcount from 45 to 19.

One of my favourite examples of this technology in use is Incio AI in the UK. I interviewed Rachel Curtis, the company's CEO, on FinTech Profile earlier this year. Inicio is a London startup whose conversational AI agent, "Budgie", handles affordability and income and expenditure ("I&E") assessments for banks, lenders, debt collectors and utilities. It is, as Inicio likes to point out, the only FCA-authorised business using AI to process consumer affordability data in the UK.

That regulatory positioning matters. Where the US firms in the Wired piece are largely competing on persistence, scale and how natural the bot sounds while it asks for money, Inicio is competing on the quality of the conversation that happens before anyone hands money over: Can a customer in financial difficulty sit down with an AI agent at 11pm and walk through their real budget without being judged, rushed or filtered through a tired call centre operator?

Their numbers are different in character too. Inicio reports completion rates above 85% on I&E assessments, agent time reduced by more than 50%, and I&E agent costs cut by up to 90%. The published end-user quotes lean heavily on customers feeling less judged talking to Budgie than to a human, which echoes what Wired heard from Floatbot's founder in the US.

What is interesting is that both ends of the market are leaning on the same psychological insight: people are often more honest with a well-designed AI than they are with a person, especially about money. Rachel put it well when we spoke earlier this year:

"Banks underestimate AI in how honest consumers are with it. In many cases, people are more open with a well-designed AI than they are with a human, particularly around sensitive financial topics."

There will always be a use, I'm sure, for general purpose AI agents - if only to receive initial calls from customers and distribute them to the right teams - however I think we'll increasingly see a lot more demand for specific, specialist agent technology like Incio.